Understanding Collections Financial Standards and IRS Regulations

- raywellman

- May 7

- 4 min read

When dealing with tax debts, understanding the financial standards and regulations set by the IRS is crucial. These rules guide how the IRS collects unpaid taxes and how taxpayers can navigate the process. This post explains the key concepts behind collections financial standards and IRS regulations, helping you grasp what to expect and how to manage your tax obligations effectively.

What Are Collections Financial Standards?

Collections financial standards are guidelines the IRS uses to determine a taxpayer’s ability to pay outstanding tax debts. These standards set limits on how much money taxpayers can reasonably spend on basic living expenses while repaying their tax debts.

The IRS uses these standards to:

Calculate allowable living expenses

Decide if a taxpayer qualifies for payment plans or offers in compromise

Determine if the IRS should delay collection actions due to financial hardship

These standards are based on national and local data about typical household expenses, including housing, utilities, food, transportation, and health care.

How the IRS Uses Financial Standards in Collections

When the IRS contacts a taxpayer about unpaid taxes, they review the taxpayer’s financial situation. The IRS compares the taxpayer’s income and expenses against the collections financial standards to see if the taxpayer can afford to pay the debt.

If the taxpayer’s expenses exceed the IRS standards, the IRS may classify the taxpayer as unable to pay, which can lead to:

Temporary delay in collection efforts

Approval of installment agreements with lower monthly payments

Consideration of an offer in compromise to settle the debt for less than owed

If the taxpayer’s income exceeds the standards, the IRS expects payment in full or through a structured payment plan.

Key Categories of IRS Financial Standards

The IRS divides financial standards into several categories to cover typical household expenses:

Housing and Utilities

This includes rent or mortgage payments, property taxes, insurance, electricity, gas, water, and phone services. The IRS provides regional allowances based on local cost of living.

Food, Clothing, and Miscellaneous

The IRS sets monthly allowances for groceries, clothing, and other necessary household items. These amounts vary by family size.

Transportation

This covers vehicle ownership costs such as loan payments, insurance, fuel, and maintenance. The IRS also allows for public transportation expenses where applicable.

Health Care

Medical and dental expenses not covered by insurance are included here. The IRS allows taxpayers to deduct reasonable out-of-pocket health care costs.

Other Necessary Expenses

This category includes child care, education, and other essential costs that the IRS recognizes as necessary for the taxpayer’s well-being.

IRS Regulations Governing Collections

The IRS follows strict regulations to ensure fair and lawful collection of tax debts. These rules protect taxpayers’ rights while allowing the IRS to recover owed taxes.

Fair Debt Collection Practices

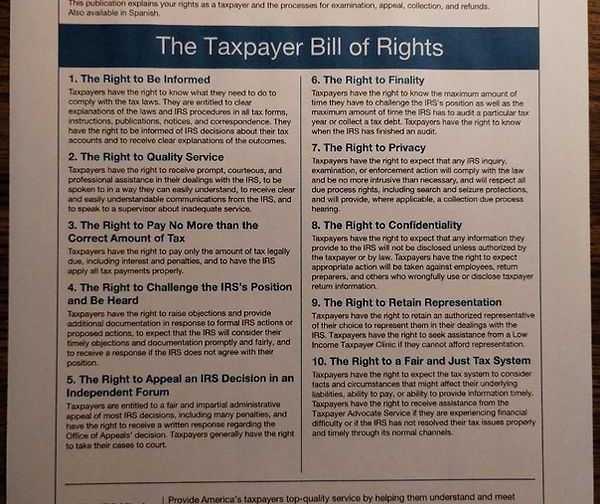

The IRS must follow the Fair Debt Collection Practices Act (FDCPA), which prohibits abusive, deceptive, or unfair collection tactics. Taxpayers have the right to:

Request verification of the debt

Be treated respectfully by IRS agents

Appeal collection decisions

Installment Agreements

The IRS offers installment agreements to taxpayers who cannot pay their tax debt in full immediately. These agreements allow monthly payments based on the taxpayer’s financial situation, often calculated using collections financial standards.

Offers in Compromise

An offer in compromise lets taxpayers settle their tax debt for less than the full amount owed if they demonstrate an inability to pay. The IRS evaluates offers based on income, expenses, asset equity, and future earning potential.

Currently Not Collectible Status

If a taxpayer cannot pay any amount without causing significant financial hardship, the IRS may place the account in currently not collectible status. This temporarily suspends collection efforts but does not erase the debt.

Practical Examples of Collections Financial Standards in Action

Example 1: John’s Installment Agreement

John owes $15,000 in back taxes but earns $3,000 per month. His allowable monthly expenses based on IRS standards total $2,500. That leaves $500 available for tax payments. The IRS approves an installment agreement requiring John to pay $500 monthly until the debt is cleared.

Example 2: Maria’s Offer in Compromise

Maria owes $30,000 but has limited income and high medical expenses. After submitting detailed financial information, the IRS determines Maria’s reasonable collection potential is $10,000. The IRS accepts her offer to settle the debt for $10,000, which she pays in a lump sum.

Example 3: Currently Not Collectible Status

David lost his job and has no income. His expenses exceed his income, and he cannot make any payments. The IRS places his account in currently not collectible status, delaying collection while David improves his financial situation.

How to Prepare for IRS Collections

Understanding collections financial standards helps taxpayers prepare for IRS interactions. Here are steps to take:

Gather financial documents such as pay stubs, bank statements, and bills

Calculate your monthly income and expenses using IRS standards as a guide

Consider consulting a tax professional to review your situation

Respond promptly to IRS notices and provide requested information

Explore payment options like installment agreements or offers in compromise

Tips for Managing IRS Collections Successfully

Keep detailed records of all communications with the IRS

Stay current on any agreed payment plans to avoid default

Notify the IRS immediately if your financial situation changes

Avoid ignoring IRS notices, which can lead to enforced collection actions

Use IRS tools and resources available online for payment plans and financial standards

Summary

Collections financial standards and IRS regulations form the foundation of how tax debts are managed and collected. These standards ensure taxpayers can meet basic living expenses while addressing their tax obligations. Knowing how the IRS applies these rules can help you navigate collections more confidently and find solutions that fit your financial reality.

If you face tax debt, take action early. Use the IRS financial standards to understand your options and communicate clearly with the IRS. This approach increases your chances of resolving your tax issues in a manageable way.